What are the key customer experience metrics in banking?

Why do NPS, CSAT, and CES matter for banking executives?

What's a good NPS score for banks and credit unions?

Benchmarking NPS in banking depends on region and market segment, but general benchmarks include:

For credit unions, NPS scores are often higher — typically ranging from 45 to 85 — reflecting stronger member relationships and local trust. Scores above 60 are generally considered excellent in that segment.

For credit unions, NPS scores are often higher — typically ranging from 45 to 85 — reflecting stronger member relationships and local trust. Scores above 60 are generally considered excellent in that segment.

A high NPS shows strong advocacy and retention potential. But success also depends on closing the loop — analyzing feedback, responding to detractors, and mobilizing promoters to share positive stories. The real power of NPS lies in its use as a catalyst for improvement rather than a static score.

How is CSAT measured in financial institutions?

What is CES and why is it critical for banking?

How do CX metrics connect to business outcomes like retention and profitability?

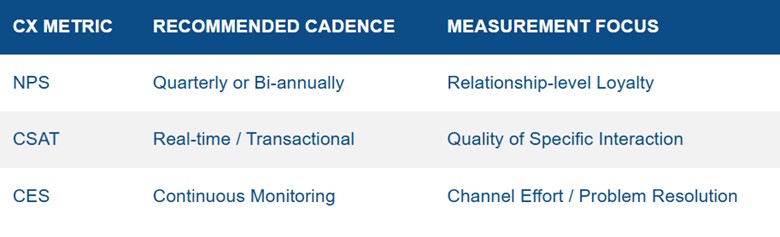

How often should banks measure and review CX metrics?

Continuous feedback is essential to stay agile. Monthly text analytics and root-cause analysis sessions help transform data into action. Executive teams should review CX dashboards at least monthly to identify emerging issues or opportunities.