CASE STUDY

MyUSA Credit Union: Neighborhood CUs Become “Better Together” at Serving Their Members

Client: MyUSA Credit Union ($336.5M assets; 9 branches; 20K members)

Industry: Credit Unions, Financial Services

Support EXP Solution: Insight Builder member survey platform

Outcomes:

- Sustainable 40-point increase in NPS from quarter following merger (4Q 2021 to 1Q 2023)

- 27% increase in Ease-of-Use Score during same period

- April 2023 General Transaction scores were the highest of the preceding 12 months

Key Takeaways:

- The success of a merger depends on leadership’s attention to execution, action, and team results – focusing on how work gets done with an execution mindset that intelligently deploys processes, tools, skills, and techniques.

- Outcomes need to be continually measured and evaluated to facilitate the informed decision-making of organizational leadership.

- Retaining members throughout a merger requires (a) anticipation of member concerns and (b) demonstration to members of both alignment in values and the capability to deliver on member expectations (e.g., speed, reliability, and ease of use).

This is a case study of two credit unions in the same Ohio community that came together to future-proof themselves against the competitive dynamics of today’s financial services environment. By adopting a strategic plan for collecting and responding to member feedback, the newly formed credit union was able to decisively recover and improve their member satisfaction following the merger.

“

"Member service is a key pillar in all that we do as a credit union. We like to say, ‘It’s about delivering the MyUSA Experience.’ For MyUSA Credit Union to achieve sustained success in communities once served by MidUSA CU and Heartland FCU, we acknowledge the need to ‘double down’ on the areas that ensure we meet our members’ expectations with expert guidance and financial tools that make a difference in our members’ lives. This is truly a combination where ‘one plus one equals the strength of three’ – and our members and communities are the beneficiaries. Every member, every experience, every time."

– James Miles, CEO of MyUSA Credit Union

Mergers Accelerating: Threat or Opportunity?

As with so many other aspects of life in recent years, rapid change has become a constant in the credit union industry.

The long-term trend toward credit union consolidation has regained momentum following a brief pandemic-induced pause. In the first quarter of 2022, the NCUA approved 41 mergers, following a year that saw a total of 161 credit union mergers. In 2022, the NCUA approved a total of 181 consolidations. Most recently, the NCUA approved 33 mergers in the first quarter of 2023 and 36 in the second. Merger and acquisition activity also now includes a variety of non-credit union entities, including community banks and fintechs, that can provide needed capabilities and resources. 2022 ended, for example, with 16 proposed bank purchases by credit unions.

What’s driving this trend? Many smaller credit unions have turned to mergers as part of their growth strategy, recognizing the need to grow rapidly to survive in a very competitive and regulation-heavy industry. Expansion through merger can be a cost-effective way to increase market share, acquire new branch locations and needed talent, and generally expand presence in a community. Institutions struggling to keep up with evolving consumer demands for improvements in digital channels, personalization, and security benefit from the efficiencies of pooled resources.

But there’s no guarantee a merger will be successful. It’s easy for merging organizations to get so caught up in addressing the seemingly endless list of integration-related tasks that the very real concerns of members – both existing and potential – are overlooked. The result: member frustration and attrition.

A merger or acquisition is a critical moment in a financial consumer’s relationship with his or her financial institution. Not only before and during the acquisition, but for a significant period afterwards, the customer’s relationship with the FI is at risk as he or she considers if they are going to remain with the new organization. “It isn’t the same since the merger,” is not something you want to hear – chances are, it’s not meant as a compliment.

Companies that prioritize the bottom line over customer satisfaction tend to suffer the greatest profit losses following a merger.[1] Loss of customer satisfaction – and the customer churn that accompanies it – can eventually overshadow the initial gains in efficiencies and cost savings.

Merging credit unions must take the member experience – and the resulting member satisfaction – into account when implementing a merger…or brace for impact. Aftershocks from undiagnosed or unaddressed issues related to the merger will continue to be felt for a long time. What are the costs of members not continuing with the “new” credit union? The risks are high, and most are not prepared to deal with the fallout.

The good news is that, done well, mergers provide opportunity: for growth, for strengthening of relationships, and for renewal of purpose in the emergence of a new brand identity.

The story that follows is a real-world example of how a merger of two credit unions can foster this opportunity and avoid the aftershocks that accompany major organizational change.

Shared Community Roots

MidUSA Credit Union, based in Middletown, Ohio, was formed in 1934 by a group of Armco Steel workers. Heartland Federal Credit Union was formed by employees of Dayton Telco in 1935. Both institutions had a passion for providing exceptional service to their members and their communities. To ensure they were meeting their members’ expectations, both credit unions separately engaged Support EXP to help measure their member experience and improve performance through feedback-driven solutions, actionable analytics, and expert, hands-on consulting.

Coming out of the COVID-19 pandemic, credit unions faced an environment full of challenges, including low net interest margins, difficulty in attracting and retaining talent, and increased competition from non-traditional players in the banking market. Storm clouds are also increasing as net revenue and non-interest income decline. Liquidity is also a challenge as consumers chase better rates.

To better solidify their position in the Dayton-area market and create a “sustainable position of strength,” MidUSA Credit Union and Heartland Federal Credit Union entered into partnership discussions. The result was the creation, on July 1, 2001, of MyUSA Credit Union.

In announcing the new entity, Jim Miles, the former CEO of MidUSA CU and CEO of MyUSA CU, noted that “MyUSA Credit Union is the culmination of combined efforts between MidUSA and Heartland to develop a unique credit union team that has the size, strength, and flexibility to meet member needs with the personalized service for which both credit unions are known.”

The strategic plan governing the merger was titled, “Better Together.” The vision of MyUSA CU’s leadership for maximizing the value of the partnership rested on the following principles:

- Creating a financial services player of size and scale in Southwest Ohio

- Providing increased value to members of both credit unions

- Giving leadership a better chance for organizational growth and success

- Giving the combined staffs better ability for career growth and prosperity

- The opportunity to sustain mutual organizational history and credit union impacts

Key Objectives for Support EXP

As a longstanding partner of both MidUSA CU and Heartland FCU, Support EXP was tasked with helping MyUSA CU reduce the disruption that accompanies most mergers. In its strategy, Support EXP proposed a plan to diagnose service issues, including member friction and lack of seamlessness in service, that members transacting business with the merging institutions might potentially encounter. By pinpointing these “hot spots” as they flared up, MyUSA CU personnel would be equipped to take timely action to retain more members of both credit unions as they assumed their new, united identity.

“In merger growth strategies, a chief asset is the gain of new members/financial consumers to strengthen market share. If the merger strategy is not carefully crafted, executed and monitored to understand these new members, as well as the impact on existing members, any hoped-for gains will end up as losses – spread out over a wider field.”

Making “Better Together” a Reality

When a company announces a merger, the natural customer reaction is uncertainty. It’s just human nature to resist the idea of change, even if the change will be beneficial in the long run. Initial analysis revealed that just floating the rumor or idea of a merger provoked an emotional response from MidUSA CU and Heartland FCU members due to uncertainty about what the future held.

For credit unions, this reaction may be multiplied depending on the length and strength of a member’s relationship with the organization. Credit unions, after all, largely define themselves by their community identity, whether based on shared geography, employment, or other affinity. Both sides of the merger may be dealing with a profound sense of loss, as they feel they are losing “their” credit union. Early comments from members of both merging institutions reflected this sense of impending loss.

Market research [2] reveals that, during a merger, banking customers are most concerned about:

- Increased prices / costs

- Diminished choice in products and services

- Reduced quality / responsiveness of customer service

- Disclosure of personal information

- Inability to transact business how they want

These fears were potential obstacles to a smooth transition for MyUSA Credit Union – a transition intended to bring members of both merging organizations into the newly formed organization. Of equal concern was the friction – both external and internal – that could materialize during the merger. Technical problems, long wait times, and lost product and service options had the potential to prompt even longstanding members to be more open to trying out the competition.

As the merger played out, member feedback revealed frustration associated with the integration of the banking systems and adoption of new procedures. MyUSA CU’s NPS took a significant hit. Was the new organization resilient enough to recover its members’ trust?

Strategy/Plan

As part of its Strategic Business Plan, MyUSA CU adopted a member service imperative based on a Relationship Banking Model [3] developed by Filene Research Group. This model is characterized by high-touch, nimble responsiveness; an organizational mission tied to community, cooperation, and commitment; alignment in values and capability to meet expectations for speed, reliability and ease of use; and personalized delivery of carefully curated products and services.

MyUSA Credit Union’s CX measurement and management strategy was based on Support EXP’s 5-Step Model for CX Success:

- DIAGNOSE CX friction preventing MyUSA CU from living up to its brand standard or to members’ changing expectations. Comprehensive measurement would reveal the gaps between the service members expected and the service they actually received.

- PRIORITIZE exact areas of focus in alignment with MyUSA CU’s business objectives. Member surveys would be used to triage MyUSA CU’s “hot spots” throughout all of their Products, Processes, People and Channels.

- FIX “hot spots” and/or systemic issues at the root level, as Support EXP’s expert analysts uncovered key themes and insights emerging from the CX data.

- ACCELERATE time to action through CX strategy informed by ongoing executive-level insight and consultation, and through as-needed assistance in the execution.

- DIFFERENTIATE by building a visible culture of service quality that grows member loyalty and sets MyUSA CU apart. This is where the new organization wanted to be!

The Approach

To meet MyUSA CU’s Key CX Objectives and retain membership through the merger, Support EXP adopted a multi-phased CX approach:

Phase 1: Substantial on Diagnostics, Agile on Action

Support EXP used post-transaction member surveys, deployed through its Insight Builder survey platform, to benchmark CX over three months starting after the merger in 2021. These surveys were used to diagnose CX issues arising from MyUSA CU’s People, Products, Processes and Channels – providing insight to inform 2022 strategy. This insight presented a concise body of data for early traction in 2022.

To ensure MyUSA CU was getting the most value from its feedback data, Support EXP conducted regular Executive Level Data Translations. In these sessions, Support EXP data analysts presented a comprehensive analysis of MyUSA CU’s member feedback metrics, as well as a comprehensive analysis of member comments and sentiment. Not only did Support EXP identify key themes and insights from MyUSA CU’s collected feedback, its leaders recommended specific action items to prioritize at the beginning of 2022 to accelerate toward meeting MyUSA CU’s identified business goals and CX objectives.

Phase 2: Substantial on Diagnostics, Weighty but Flexible on Action

Support EXP continued post-transactional member surveys to diagnose CX issues arising from MyUSA CU’s People, Products, Processes and Channels. Through Support EXP’s Actionable Analytics Portal, MyUSA CU had access to its collected member feedback data through high-level dashboards, segmented analysis, and real-time executive view of their CX as delivered through their People, Products, Processes and Channels.

Support EXP’s data analysts also continued to perform a comprehensive analysis of each month’s CX feedback metrics from CX surveying, including review of drivers and sub-drivers across Products, Processes, People, and Channels. This approach informed MyUSA CU’s response to indications of member dissatisfaction. The Call Center, for example, is an important touchpoint for MyUSA CU members, as evidenced by driver and subdriver analysis. Although the Call Center’s NPS dipped to a low of 33.33 in December 2022, working through Support EXP’s 5-Step Model from Diagnosis to Differentiation, brought MyUSA CU’s Call Center NPS up to 95.24 in May 2023 – exceeding the previous high of either MidUSA CU or Heartland FCU. That is what “better together” looks like in action!

Support EXP data analysts also conducted a comprehensive analysis of member comments and sentiment and provided a monthly KPI performance tracker to monitor key CX metrics against defined targets, based on MyUSA CU’s CX strategic initiatives and defined priorities.

Senior strategists of Support EXP formally presented key insights from feedback data analytics to MyUSA CU’s C-Level, and other selected stakeholders. These working sessions brought to light specific trends and “hot spots” for senior leaders to prioritize for action to inform/adjust CX strategy, focus operational resources and/or change CX practices directly related to MyUSA CU’s key CX objectives.

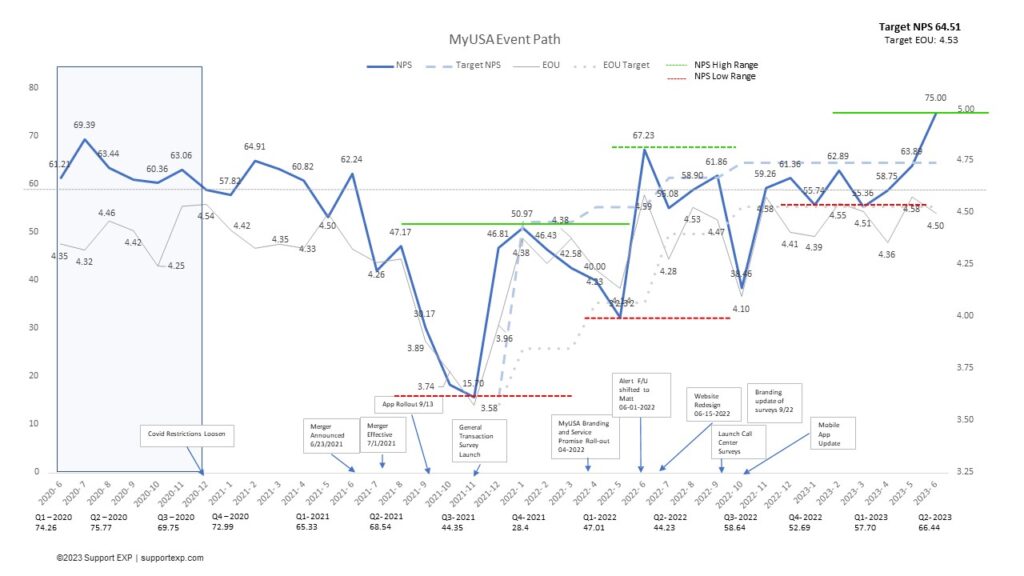

As part of its data translation, Support EXP analysts constructed an “Event Path” showing trends in MyUSA CU’s CX metrics plotted along a timeline of events with potential impact on its members’ relationship with and perception of the credit union. The Event Path tracked the resilience of MyUSA CU in boosting its NPS from a post-merger low of 15.70 to a sustained NPS in the 55-65 range (see illustration below). While reflecting the volatility so common in customer feedback, the trend in CX scores ultimately showed the outcomes of MyUSA CU’s commitment to listening to, and acting on, its member feedback.

Support EXP representatives also assisted MyUSA CU with Alert Management services, stepping into the role of “first responder” to expertly handle initial responsibilities of member connection and triage of service recovery, set up the “case” in the EXP Actionable Analytics Portal, hand off connection to MyUSA CU for follow-up while tracking the case through to closed status, as defined by MyUSA CU’s business rules.

Outcomes

According to MyUSA Credit Union’s leadership, the partnership of Heartland FCU and MidUSA CU created a sustainable position of strength in their newly shared community.

The two institutions relied on the following objectives to optimize the value of their partnership:

- Creating a financial services player of size and scale in Southwest Ohio

- Providing increased value to members of both credit unions

- Giving leadership a better chance for organizational growth and success

- Giving the combined staffs better ability for career growth and prosperity

- The opportunity to sustain mutual organizational history and credit union impacts

As a result of following these principles, MyUSA CU achieved more “mass” to compete and invest in today’s market. MyUSA is sustainably stronger and better equipped to face economic and competitive challenges. MyUSA CU is a successful financial cooperative that will make a difference in the long term for the communities it serves, will provide rewarding work and careers for its employees, will live up to the promise of “people helping people,” and will actively participate with the credit union cooperative spirit.

Conclusion

No matter their size, merging credit unions thrive only when they have a clear line of sight around the member and employee experiences, and are equipped to act in such a way that their greatest asset, their members, are never at risk of going elsewhere.

As shown in the case of MyUSA Credit Union, sound strategy for collecting member feedback at all crucial touchpoints and phases of a merger can give you an essential picture of your members’ and employees’ expectations throughout the process. By better understanding your members, you can make the merger experience easier and more predictable for both you and them, building the trust that will keep your members loyal over time.

The transformation of MidUSA CU and Heartland FCU into a single, unique organization could only be done by the leaders and employees of those organizations and their commitment to the vision of “Better Together.” In that spirit, Support EXP was proud to assist in the transformation, positioning MyUSA CU’s executives to effect the change they wanted by providing a data-driven clear line of sight.

MyUSA CU’s partnership with Support EXP enabled the new credit union to:

- Focus more time and energy on the actual merger and the numerous associated tasks

- Ensure the merging companies focused their time and energy on root causes of problems and issues as identified in MX and EX feedback

- Strengthen member acceptance, engagement and loyalty with the new organization

As with so many other areas, the success of a merger like that undergone by MyUSA CU depends on effective execution. Demonstrating top-down support for the change, establishing clear accountability for the integration, and providing support from the back office to the frontline sets the stage for sound execution and success.

Support EXP Solution: Insight Builder

Net Promoter®, NPS®, NPS Prism®, and the NPS-related emoticons are registered trademarks of Bain & Company, Inc., Satmetrix Systems, Inc., and Fred Reichheld. Net Promoter Score℠ and Net Promoter System℠ are service marks of Bain & Company, Inc., Satmetrix Systems, Inc., and Fred Reichheld.

[1] Umashankar, Nita, et al., “Despite Efficiencies, Mergers and Acquisitions Reduce Firm Value by Hurting Customer Satisfaction,” Journal of Marketing, Oct. 5, 2021.

[2] See, e.g., Schaus, Paul. “After Acquisition, It’s All About Customers.” Banking Exchange, October 21, 2016. https://m.bankingexchange.com/news-feed/item/6527-after-the-acquisition-it-s-all-about-customers